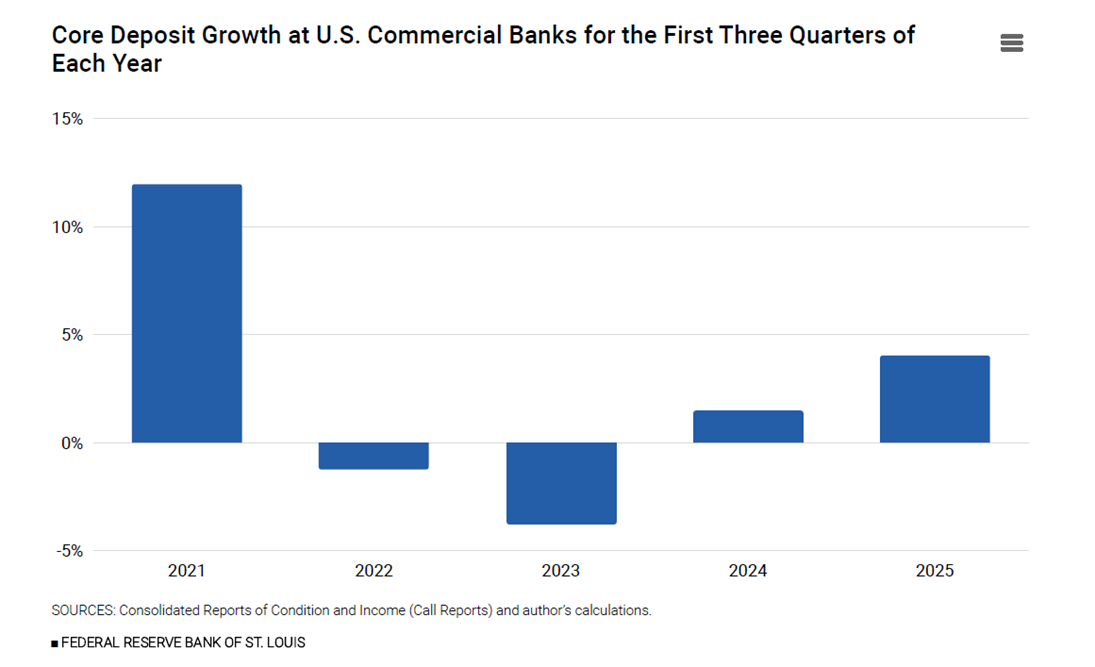

Core deposit growth at U.S. commercial banks accelerated in the first three quarters of 2025, by about 4% compared with 1.5% through the first three quarters of 2024. This was a welcomed improvement given that lending by banks also was higher in 2025, and banks use deposits to fund loans.

Generally, core deposits include stable, lower-cost funding sources that typically lag other funding sources in repricing during a period of rising interest rates. They ideally represent funds belonging to local customers that also have a borrowing or other relationship with the bank.

There are several factors that may influence the stability of core deposits, such as the insured status of the account and the type of depositor. The figure below reflects total core deposits, which include checking and savings accounts, money market deposit accounts, and fully insured certificates of deposit (i.e., time deposits of $250,000 and less).

2025’s growth rate of 4.0% improves from 1.5% in 2024 and negative growth rates realized through the first three quarters of 2023 and 2022.

Core deposits grew by nearly 12% through the first nine months of 2021 as COVID-19 pandemic-era stimulus funds entered the banking system. Some of those funds exited the banking system in the following years, but core deposits appear to be growing again.

There are several factors that influence deposit trends, including fiscal stimulus (mentioned above), interest rate dynamics, economic stability and deposit competition. For example, falling interest rates may make bank products more competitive than other investments, thereby boosting deposits. Other times, uncertainty prompts a “flight to safety” into banks where consumer and business clients can closely monitor their funds.