This series is part of ongoing work by the Supervisory Policy and Risk Analysis team to highlight key banking metrics in monitoring the health of the banking system, a function of the St. Louis Fed’s Supervision, Credit and Learning Division.

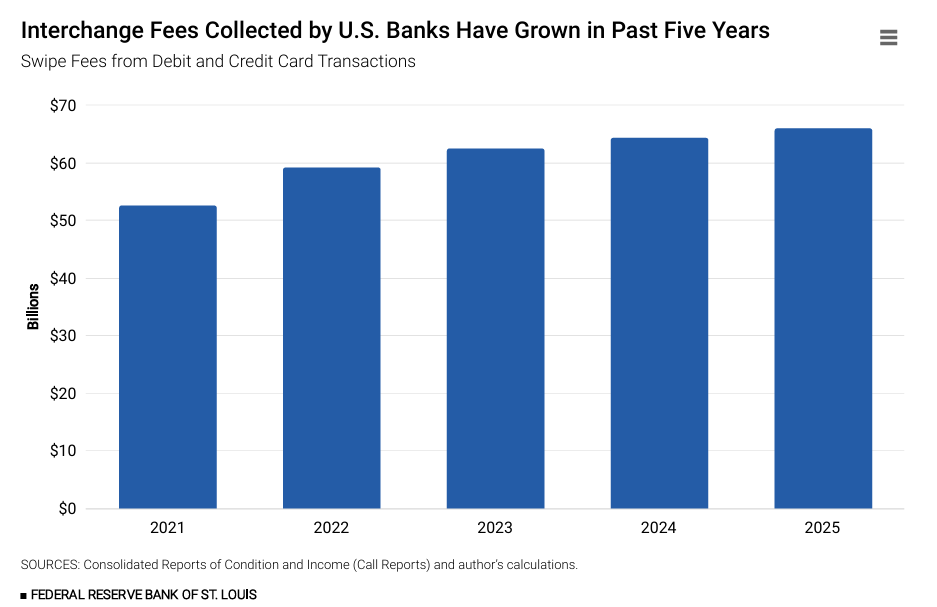

U.S. banks collected nearly $66 billion in interchange, or “swipe,” fees in 2025, up from $64 billion in 2024 and $52 billion in 2021. (See figure below.) Factors that influence the volume of interchange revenues collected by banks include card usage, the price level of purchased goods and services, alternative payment options and overall economic conditions.

Debit and Credit Card Purchase Volumes Have Been Growing

Furthermore, both debit and credit card purchase volumes have been increasing in recent years, according to the Large Bank Credit Card and Mortgage Data 2025 Q3 Narrative. For credit card transactions, the average purchase volume per account continued to increase year over year within all credit score bands through the third quarter of 2025, the report said. Similarly, a 2025 Federal Reserve Board report (PDF) found that both total debit card transaction volume and value grew at an average annual rate of 4.6% from 2021 to 2023.

How Interchange Fees Work, and Why They Matter for Banks

Interchange fees are fees paid between banks so that merchants can accept card-based transactions on behalf of consumers. Every time a consumer makes a purchase using a debit or credit card, the bank that issued the card pays the merchant’s bank on the consumer’s behalf. The amount the merchant receives, however, is not simply the price of the product or service, but a lesser amount that reflects transaction fees paid to the card payment firms and banks involved in the transaction. This includes the interchange fee that is paid to the bank that issued the credit or debit card used by the consumer in the transaction.

Interchange fees remain an important source of income for banks, equating to approximately 11% of noninterest income for U.S. banks in 2025, up from 9% in 2021. Banks then use these fees to cover the costs of authorizing new cards, processing and settling transactions, providing fraud protection and operating rewards programs.