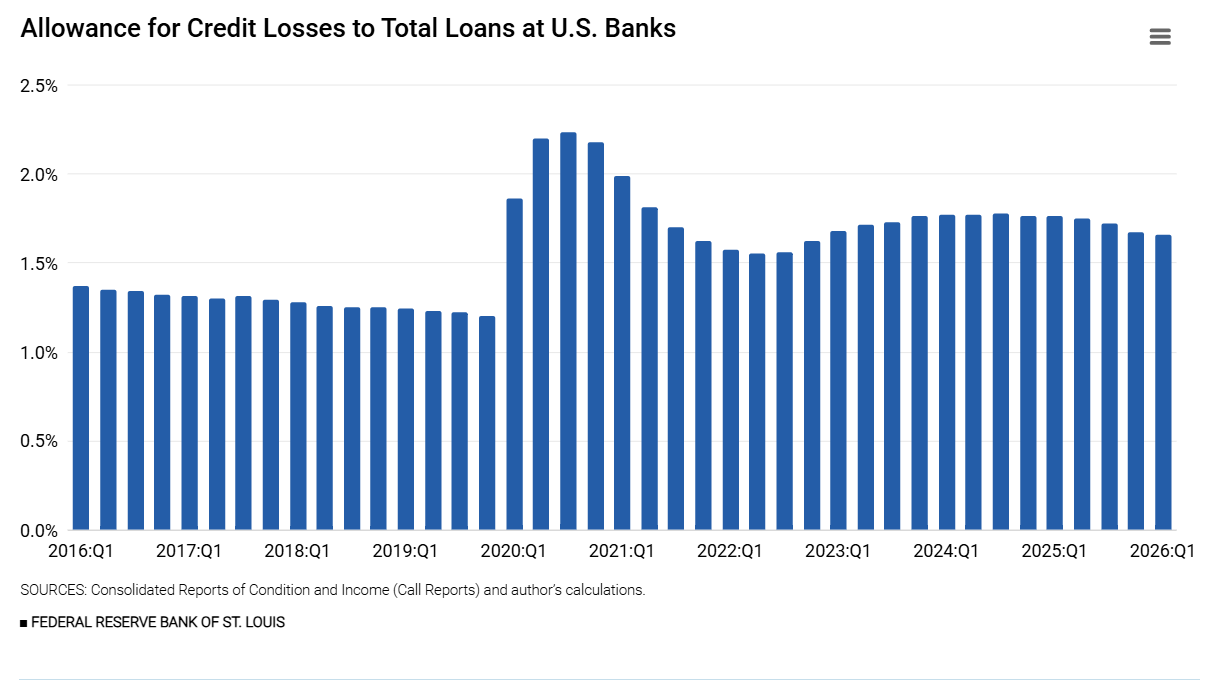

he allowance for credit losses (ACL) coverage ratio for the U.S. banking system remained stable in the first quarter of 2026, decreasing slightly to 1.66% from 1.67% in the preceding quarter.1 (See the figure below.) The ACL coverage ratio has declined gradually over the past six quarters from a recent peak of 1.78% at the end of the third quarter of 2024.

Every time a bank makes a loan, there is some likelihood that a percentage of the loan will not repay. To account for those potential defaults, banks establish loan loss reserves by debiting the income statement expense account “provision for credit losses” while crediting the balance sheet account “allowance for credit losses.”2

In recent years, banks have experienced overall controlled rates of loan delinquencies and charge-offs, which has kept provision expenses (as a percentage of loans and leases) stable.

What ACL Coverage Ratios Tell Us

Banks and regulators closely watch the ratio of ACL to total loans and leases because it reveals important insights about a bank’s loan portfolio and risk assessment. A high ACL coverage ratio suggests that a bank expects high loan losses ahead. This could indicate a riskier loan portfolio, economic pessimism about borrowers’ ability to repay or deteriorating loan quality in the existing portfolio. A low ACL coverage ratio suggests that a bank is expecting fewer losses, which might mean a higher-quality loan portfolio, economic optimism about repayment prospects, strong collateral backing the loans or underestimation of projected credit losses.

Neither a high nor a low ACL coverage ratio is inherently good or bad. The appropriate level varies for every bank depending on its lending strategy, the economic environment and the types of loans issued. For instance, in 2020, during the COVID-19 pandemic, banks greatly increased their ACL because of a spike in economic uncertainty, with the ACL coverage ratio peaking 2.23%. (See the figure above.) As conditions improved, ACL coverage ratios declined. For the public, monitoring ACL coverage ratios across banks provides insight into how financial institutions view economic health and lending risk.

Sudden increases in ACL coverage ratios may signal higher uncertainty or economic trouble ahead, while decreases might indicate improving confidence. Today, banks do not appear to be making significant adjustments despite elevated levels of economic uncertainty.

Notes

The ACL coverage ratio is defined as banks’ allowance for credit losses to total loans and leases.

The “allowance for credit losses” valuation account is measured as the difference between financial assets’ amortized cost basis and the amount expected to be collected on financial assets. See the Financial Accounting Standards Board’s Accounting Standards Update No. 2016-13, “Measurement of Credit Losses on Financial Instruments” (PDF) for a detailed description of ACL accounting standards.